GST collection crosses Rs.1.40 lakh crore mark 4th time since inception of GST; 3rd month at a stretch since March, 2022 The gross GST revenue collected in the month of May, 2022 is Rs.1,40,885 crore of which CGST is Rs. 25,036 crore, SGST is Rs.32,001 crore, IGST is Rs.73,345 crore (including Rs. 37469 crore collected on import of goods) and cess is Rs. 10,502 crore (including Rs. 931 crore collected on import of goods).

GST Revenue collection for May, 2022

Rs. 1,40,885 crore gross GST Revenue collection for

May, 2022; increase of 44% year-on-year

GST collection crosses Rs.1.40 lakh crore mark 4th time since inception of GST; 3rd month at a stretch since March, 2022 The gross GST revenue collected in the month of May, 2022 is Rs.1,40,885 crore of which CGST is Rs. 25,036 crore, SGST is Rs.32,001 crore, IGST is Rs.73,345 crore (including Rs. 37469 crore collected on import of goods) and cess is Rs. 10,502 crore (including Rs. 931 crore collected on import of goods).

The Government has settled Rs.27,924 crore to CGST and Rs.23,123 crore to SGST from IGST. The total revenue of Centre and the States in the month of May, 2022 after regular settlement is Rs.52,960 crore for CGST and Rs.55,124 crore for the SGST. In addition, Centre has also released GST compensation of Rs.86912 crores to States and UTs on 31.05.2022.

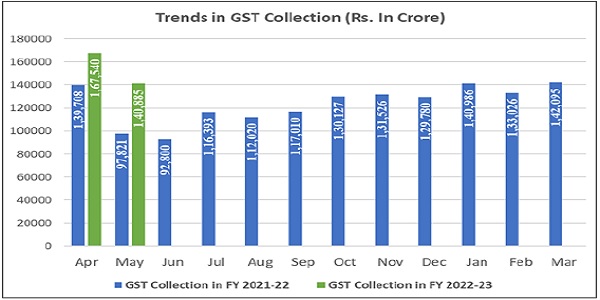

The revenues for the month of May, 2022 are 44% higher than the GST revenues in the same month last year of Rs.97,821 crore. During the month, revenues from import of goods was 43% higher and the revenues from domestic transaction (including import of services) are 44% higher than the revenues from these sources during the same month last year.

This is only the fourth time the monthly GST collection crossed Rs.1.40 lakh crore mark since inception of GST and third month at a stretch since March, 2022. The collection in the month of May, which pertains to the returns for April, the first month of the financial year, has always been lesser than that in April, which pertains to the returns for March, the closing of the financial year. However, it is encouraging to see that even in the month of May, 2022, the gross GST revenues have crossed the Rs.1.40 lakh crore mark. Total number of e-way bills generated in the month of April, 2022 was 7.4 crore, which is 4% lesser than 7.7 crore e-way bills generated in the month of March, 2022.

The chart shows trends in monthly gross GST revenues during the current year.

Source: PIB Press Release dated 01. 06.2022

Press Release

Centre Clears Entire GST Compensation Due till Date

(31st MAY, 2022)

The Government of India has released the entire amount of GST compensation payable to States up to 31st May, 2022 by releasing an amount of Rs. 86,912 crores. This decision was taken to assist the States in managing their resources and ensuring that their programmes especially the expenditure on capital is carried out successfully during the financial year. This decision has been taken despite the fact that only about Rs. 25,000 crore is available in the GST Compensation Fund. The balance is being released by the Centre from its own resources pending collection of Cess.

Goods and Services Tax was introduced in the country w.e.f. 1st July, 2017 and States were assured for compensation for loss of any revenue arising on account of implementation of GST as per the provisions of the GST (Compensation to States) Act, 2017 for a period of five years. For providing compensation to States, Cess is being levied on certain goods and the amount of Cess collected is being credited to Compensation Fund. Compensation to States is being paid out of the Compensation Fund w.e.f. 1st July, 2017.

Bi-monthly GST compensation to States for the period 2017-18, 2018-19 was released on time out of the Compensation Fund. As the State's protected revenue has been growing at 14% compounded growth whereas the Cess collection did not increase in the same proportion, COVID-19 further increased the gap between protected revenue and the actual revenue receipt including reduction in cess collection.

In order to meet the resource gap of the States due to short release of compensation, Centre has borrowed and released Rs.1.1 lakh crore in 2020-21 and Rs.1.59 lakh crore in 2021-22 as back-to-back loan to meet a part of the shortfall in Cess collection. All the States have agreed to the above decision. In addition, Centre has also been releasing regular GST compensation from the Fund to meet the shortfall.

With the concerted efforts by Centre and States, gross monthly GST collection including Cess has been showing a remarkable progress. The details of GST compensation payable for the past financial years and for the period of April-May of the current financial year are given as per the table below: –

With this release of Rs. 86,912 crore, the compensation to States till May, 2022 gets fully paid and only compensation for June 2022 would remain.

STATE-WISE BREAK-UP (Amount Rs. In Crore)

Source: PIB Press Release dated 31. 05.2022

Notification

> Notification No. 05/2022 – Central Tax dated 17.05.2022 seeking extension of the due date of filing FORM GSTR-3B for the month of April, 2022.

The Government vide the said notification has extended the due date for filing FORM GSTR-3B for the month of April, 2022 till 24th May, 2022. The original due date for filing FORM GSTR-3B for April, 2022 was 20th May, 2022.

Section 39 of the Central Goods and Services Tax ('CGST') Act, 2017 provides that every registered person is required to file a monthly return electronically. The particulars such as outward supplies of goods or services, input tax credit availed, tax payable, tax paid, etc. are required to be declared in such return. However, a certain class of registered persons are required to furnish the return quarterly. In this regard, Rule 61 of the CGST Rules, 2017 prescribes Form GSTR 3B which is required to be filed by the registered person, monthly or quarterly, as the case may be.

> Notification no. 06/2022-Central Tax dated 17.05.2022 seeking extension of the due date of payment of tax, in FORM GST PMT-06.

The Government with this notification seeks to extend the due date of payment of tax, in FORM GST PMT-06, for the month of April, 2022 by taxpayers who are under Quarterly Return Monthly Payment (QRMP) scheme. Vide the said notification the government has extended the due date of payment of tax for the month of April, 2022 by taxpayers under QRMP scheme in FORM GST PMT-06 till 27th May, 2022. QRMP Scheme allows the registered person to furnish return quarterly along with the monthly payment of tax by a simple challan in FORM GST PMT-06, with effect from January 01, 2021.

> Notification no. 07/2022-Central Tax dated 26.05.2022 seeking to waive off late fee under section 47 of the CGST Act 2017.

The Government with this notification seeks to waive off late fee under Section 47 of the CGST Act 2017 for the period from 01.05.2022 till 30.06.2022 for delay in filing FORM GSTR-4 for FY 2021-22. Form GSTR-4 (Annual Return) is an yearly return to be filed once, for each financial year, by the taxpayers who have opted for composition scheme during the financial year, or were in Composition scheme for any period, during the said financial year, from 1st April, 2019 onwards.

Section 47 of the CGST Act 2017 mandates that any registered person who fails to furnish the details of outward or supplies required under section 37 or returns required under section 39 or section 45 [or section 52] by the due date shall pay a late fee of one hundred rupees for every day during which such failure continues subject to a maximum amount of five thousand rupees. Further, the section mandates that any registered person who fails to furnish the return required under section 44 by the due date shall be liable to pay a late fee of one hundred rupees for every day during which such failure continues subject to a maximum of an amount calculated at a quarter per cent. of his turnover in the State or Union territory.

GST Portal Updates

> Annual Aggregate Turnover (AATO) computation for FY 2021-22

The functionality of AATO for the FY 2021-22 has now been made live on taxpayers' dashboards with the following features:

- The taxpayers can view the exact Annual Aggregate Turnover (AATO) for the previous Financial Year (FY).

- The taxpayers can also view the Aggregate Turnover of the current FY based on the returns filed till date.

- The taxpayers have also been provided with the facility of turnover updation in case taxpayers feel that the system calculated turnover displayed on their dashboard varies from the turnover as per their records.

- This facility of turnover update shall be provided to all the GSTINs registered on a common PAN. All the changes by any of the GSTINs in their turnover shall be summed up for computation of Annual Aggregate Turnover for each of the GSTINs.

- The taxpayer can amend the turnover twice within the month of May, 2022. Thereafter, the figures will be sent for review of the Jurisdictional Tax Officer who can amend the values furnished by the taxpayer wherever required.

Note: For more details, the taxpayers may check out the 'Advisory' section of the aforementioned functionality on their respective dashboards.

> Module wise new functionalities deployed on the GST Portal for taxpayers

Various new functionalities are implemented on the GST Portal, from time to time, for GST stakeholders. These functionalities pertain to different modules such as Registration, Returns, Advance Ruling, Payment, Refund and other miscellaneous topics. Various webinars are also conducted as well informational videos prepared on these functionalities and posted on GSTNs dedicated YouTube channel for the benefit of the stakeholders.

> Addition of 6% tax rate in GSTR-1 online

- It may be noted that 6% tax rate has been added in the item details section of all the tables of form GSTR-1, except HSN table 12. In case outward supplies attract 6% tax rate, taxpayers are required to upload the details against 6% tax rate in the item details section.

- In respect to HSN table 12 of form GSTR-1, 6% tax rate shall be added shortly. Meanwhile, the HSN details of supplies attracting 6% tax rate may be reported under tax rate 5% by updating the values/tax amounts as per the actual supplies made.

Best Practices by States

> Conference on Taxpayer Friendly Measures in GST & launch of Haryana GST Returns Scrutiny Manual

The Excise and Taxation Department hosted a conference to discuss re-engineering of internal processes to improve taxpayer experience of GST taxpayers and launch of Haryana GST return Scrutiny Manual. The meeting was chaired by Sh. Dushyant Chautala, Hon'ble Dy. Chief Minister, Haryana along with Sh. Anurag Rastogi, IAS, ACS (E&T) and Sh. Shekhar Vidyarthi, IAS, Excise and Taxation Commissioner along with all officers with the rank of DETC and above posted in the Department. The following decisions were taken in the conference for better transparency and accountability: –

1. Ensuring authenticity of communication to taxpayers: – All statutory letters and communication sent to taxpayers shall be sent with an electronic ID generated through the GST common portal or through E-Office.

2. Visiting premises of taxpayers with proper authorization: – All officials shall visit the premise of a taxpayer with proper identity cards and authorization as mandated by the HGST Act, 2017.

3. Reasonable opportunity to be heard to be given to complainants – While conducting any enquiry a reasonable opportunity of being heard should be given to the complainant. However, the practice of repeated summons and calling for records from the complainant shall be discouraged.

4. Utmost caution to be exercised in blocking of Input tax credit of taxpayers: – Field formations shall exercise utmost caution and care while blocking input tax credit of taxpayers. Seniors officers shall regularly review blocking of credit as per prevailing instructions. 5. Incentive scheme for taxpayers and tax officers: – Hon'ble Deputy Chief Minister announced that a special scheme may be devised for incentivizing performance of officers and also recognition of top taxpayers for the State.

6. Launch of GST returns Scrutiny Manual for the State: – Hon'ble Deputy Chief Minister launched the GST returns scrutiny manual which consisted of detailed process to be followed by proper officers for taking up return scrutiny. The manual is one of the most comprehensive scrutiny manuals released by any State for GST return scrutiny. Hon'ble Minister was apprised that the complete process of return scrutiny, taxpayer communication, issuing of notices and monitoring and review is now online.

Source: Government of Haryana Press release dated 10.05.2022

> The Haryana Government issued instructions vide Memo No. 367/GST-2 dated May 24, 2022, regarding the processing of applications for registration in FORM GST REG 01.

The abovementioned memo mentions that while there is an urgent need of weeding out bogus / fake firms set up for passing of fake input tax credit, there is also a need of facilitating bonafide taxpayers for GST registrations. The following instructions were issued: –

a) All applicants for registration are to be processed in accordance with provisions laid down in Section 25 and Rules framed there under.

b) The Act does not mandate physical appearance / personal statements of the applicants at the time of processing of registration. This practice shall be discouraged. However, in case of doubt/suspicion, physical verification of the business premises may be conducted under Rule 25 of the HGST Rules, 2017.

c) The list of documents to be uploaded with the application for registration are already provided in FORM GST REG-01. Ideally, no extraneous information/documents shall be sought by the Proper Officer while processing such applications. However, in case of doubt/suspicion, the proper officer may call for information as he may deem fit but information shall be relevant to the application and frivolous / extraneous information shall not be called for.

Source: Government of Haryana Press release dated 24.05.2022

> The Bihar Government has launched a detailed standard operating procedure for GST audit by Departmental officers in the course of Audit under Section 65 of the BGST Act. A brief summary of the SOP released is provided herein below.

Audit is the process of examining data, information, records, documents and accounts with a view of determining the accuracy and reliability of such data, information, records, documents and accounts. In a financial framework auditing is a systematic and independent examination of the books and records of an entity with a view to verifying the completeness and accuracy of the financial records and the level of compliance of the entity with standard norms.

In the context of GST, 'the systematic and independent examination of the books and records may be limited to transactions and performances of an entity for a stated purpose, say GST. Such an audit may be conducted to ascertain whether they present a true and fair view of the financial transactions vis-a-vis returns filed with the authorities.'

Audit Procedure and Methodology

Every audit is unique since the audit depends on the fact and circumstances of each taxpayer and such facts and circumstances are never identical for any two or more taxpayers. However, professional bodies in India as well as internationally have, over the years, evolved a standard approach to the conduct of audit in a given legal regulatory framework.

(a) Assessing the tax risks and determining the extent, scope and focus of the audit.

(b) Preparation of audit plan/audit program and conduct of the audit

(c) Sampling: The audit team should also draw samples of transactions to be examined in detail and be subject to cross verification from external and internal evidences.

Conducting the Audit: This is the crux of the entire audit process and hence the most important step. After the desk review as aforesaid, notice to the auditee may be issued and a questionnaire may be appended to the said notice, directing the taxpayer to furnish answers/information regarding questions/issues that may apply to him an indicative list of books/documents/records required to be produced may also be appended by way of signed annexure to the said notice. It is advisable to conduct a desk audit in the office of the audit team by calling for relevant records and documents. Initially, all such information and records may be scrutinized in the office and the audit checks may be applied accordingly. During the process of such examination, the taxpayer may be afforded opportunity to present his case and explanation. The books/documents/records examined, tests carried out and explanation provided by the taxpayer must be duly recorded in the official audit record of the taxpayer being audited. Further, if during the course of the desk audit, if it is felt necessary to visit the place/s of business, the head of the audit team may, upon necessary approval from the concerned Additional Commissioner, proceed to such place/s. Before undertaking the field visit, the kind of checks and tests that are to be carried out must be planned.

(e) Review meeting with the audit team: The head of the audit team may conduct review meetings with the various audit teams under him and is expected to guide the team members on maintaining a focused approach. The concerned Additional Commissioner should also undertake periodic review of the activities and progress of various teams functioning under him.

(f) Formulating findings of the audit, drawing conclusions on the basis of audit evidence and other information gathered during the audit:

(g) Maintaining a record regarding all audits conducted.

The main objective of audit is to ascertain the correctness of the:

(a) turnover declared (which determines the output tax or tax payable),

(b) input tax credit availed (which determines the maximum amount of created which can be utilized for payment of the output tax or tax payable),

(c) taxes paid (which is a function of both the output tax or tax payable and the input tax credit utilized which, in turn, is limited by the input tax credit availed), and

(d) refund claimed which is-

- the difference between tax payable and tax actually paid, or

- the tax paid in cash on a zero-rated supply, or

- the un-utilized input tax credit on account of zero-rated supplies or inverted-rate structure supplies in which the credit accumulates on account of the rate of tax on inputs (input services and capital goods not to be included herein) being higher than the rate of tax on output supplies.

Accordingly, the audit team is required to carry out compliance verification in general and to ascertain whether correct tax liability has been discharged by the taxpayer.