Karnataka State Chartered Accountants Association (KSCAA) has addressed a representation to Smt. Nirmala Sitharaman, Union Minister of Finance and Chairperson of the GST Council, highlighting issues related to mandatory pre-deposits and ambiguities in pre-deposit requirements for appeals before the GST Tribunal. Established in 1957, KSCAA advocates for Chartered Accountants and the business community, aiming to resolve professional challenges through dialogue with regulatory bodies.

Karnataka State Chartered Accountants Association (KSCAA) has addressed a representation to Smt. Nirmala Sitharaman, Union Minister of Finance and Chairperson of the GST Council, highlighting issues related to mandatory pre-deposits and ambiguities in pre-deposit requirements for appeals before the GST Tribunal. Established in 1957, KSCAA advocates for Chartered Accountants and the business community, aiming to resolve professional challenges through dialogue with regulatory bodies.

The main concern raised is the financial burden imposed by the current pre-deposit requirements for GST appeals. Taxpayers are obligated to deposit 10% of disputed tax for appeals at the First Appellate Authority and an additional 20% for appeals at the GST Tribunal, totaling a significant 30% pre-deposit. This requirement places undue strain on taxpayers, hindering their liquidity and potentially exacerbating financial challenges during litigation.

Further complicating matters is the ambiguity surrounding the interpretation of pre-deposit requirements. The text of the law suggests two possible interpretations, leading to confusion about the exact amount taxpayers are required to deposit. This ambiguity could result in overpayments or underpayments, creating further financial and administrative burdens for taxpayers navigating the appeals process.

In response, KSCAA has proposed reducing the total pre-deposit requirement to 15% of the remaining disputed tax amount, thereby easing financial pressures on taxpayers. Additionally, they request clarification from the GST Council to ensure a uniform interpretation and application of pre-deposit rules across appeals to the GST Tribunal. Such measures, they argue, would promote fairness, transparency, and efficiency within the tax dispute resolution framework, benefiting both taxpayers and the broader business community in Karnataka.

Overall, KSCAA appeals to the Union Minister of Finance for consideration of their proposals, emphasizing the need for immediate action to alleviate financial hardships and streamline the appeals process under GST laws.

Karnataka State Chartered Accountants Association

To,

Smt. Nirmala Sitharaman,

Hon. Union Minister of Finance and Chairperson of GST Council, Government of India

Date: 17th June 2024

SUB: REPRESENTATION FOR REDUCTION OF MANDATORY PRE-DEPOSIT AND AMBIGUITY REGARDING PRE-DEPOSIT REQUIREMENT FOR APPEAL BEFORE GST TRIBUNAL

The Karnataka State Chartered Accountants Association (R) (in short 'KSCAA') is an association of Chartered Accountants, registered under the Karnataka Societies Registration Act, in the year 1957. KSCAA is primarily formed for the welfare of Chartered Accountants and represents before various regulatory authorities to resolve the professional problems faced by Chartered Accountants and the business community.

In the past, we have written to your good selves many times populating various issues, challenges and hardships being faced by taxpayers and Chartered Accountants and suggesting possible solutions on the same. Herein, we are presenting before your good selves for your kind consideration, an issue concerning the mandatory pre-deposit requirement for filing an appeal before the GST Tribunal. This matter has created considerable financial strain on the litigants apart from the ambiguity on the computation part of the said amount, among taxpayers and practitioners alike.

ISSUE AT HAND:

1. Addressing Financial Burden in GST Appeals: Request for Pre-Deposit Reduction

The implementation of the GST law has encountered various challenges, including typographical errors, procedural lapses, inaccuracies in disclosing of the correct values in appropriate columns of the GST returns etc. These errors, often stemming from unintentional human mistake, have contributed to an increase in unintended litigation between the tax payer and the tax authorities. Despite taxpayers demonstrating their lack of actual liability or timely payment of applicable taxes to revenue authorities, unresolved demands by the Proper Officer have exacerbated these disputes.

Presently, taxpayers are required to make a pre-deposit of 10% of the disputed tax to appeal before the First Appellate Authority. Additionally, an extra 20% of the remaining disputed tax amount must be deposited to appeal before the Appellate Tribunal. This cumulative 30% pre-deposit obligation places significant financial strain and liquidity challenges on taxpayers.

It's crucial to address these issues to ensure fairness and efficiency within the tax system. Reducing the pre-deposit requirement for filing appeals before the Appellate Tribunal could indeed alleviate the financial strain on taxpayers while also potentially streamlining the appeals process. Advocating for this change before the GSTN council to reduce the pre-deposit to a total of 15% of the remaining disputed tax amount (including the pre-deposit made at first appeal stage) could provide relief to taxpayers facing financial constraints, when filing appeals could be a constructive step towards addressing these concerns and fostering a more equitable and accessible appeal process. It may also help reduce unintended litigation and promote smoother interactions between taxpayers and tax authorities

2. Resolving Ambiguity in Pre-Deposit Requirements for GST Tribunal Appeals: Clarifying Interpretations and Implications

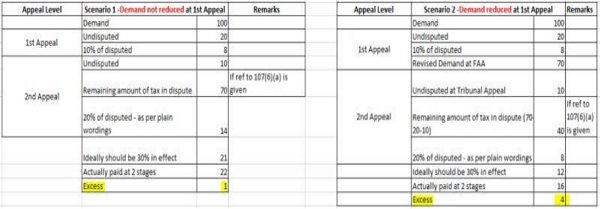

The ambiguity revolves around the interpretation of the pre-deposit requirement for appeals to the GST Tribunal. The discussions and intent of the 7th GST Council meeting suggest a pre-deposit of 30%, whereas the current wording of the law presents two possible interpretations:

Extract of the Relevant provision relating to pre deposit for preferring appeal against the order in appeal passed under section 107(11) of the CGST Act, 2017 before the Hon'ble Appellate Tribunal under section 112 (8) of the CGST Act, 2017

112. Appeal to Appellate Tribunal

..

..

(8) No appeal shall be filed under sub-section (1), unless the appellant has paid––

(a) in full, such part of the amount of tax, interest, fine, fee and penalty arising from the impugned order, as is admitted by him, and

(b) a sum equal to twenty per cent. of the remaining amount of tax in dispute, in addition to the amount paid under sub-section (6) of section 107, arising from the said order, [subject to a maximum of fifty crore rupees] , in relation to which the appeal has been filed.

There could be different interpretations arising out of the above, which is as follows:

Interpretation A:

10% of the initial demand paid at the First Appellate (FA) stage.

An additional 20% of the subsequent demand as per the FA order.

Interpretation B:

10% of the initial demand paid at the FA stage.

The amount required to reach a total of 30% of the tax demand as per the FA order.

IMPLICATIONS:

If Interpretation A is followed, it results in a compounded financial burden on the litigant, which may exceed the intended 30% pre-deposit, thereby placing an undue financial strain on taxpayers.

Interpretation B aligns more closely with the intent of the GST Council's discussions, ensuring that the total pre-deposit does not exceed 30% of the tax demand, which is a fairer and more consistent approach. A comparison of these two interpretations are given below:

As can be seen from the above comparison, the literal interpretation would lead to higher pre-deposit and in instances where substantial relief is provided at first appeal, there is a chance that the amount of pre-deposit would be more than the demand amount itself. This would impose a significant burden on litigants who are already struggling with delays in the formation of the tribunal and increasing demands over time.

REQUEST FOR CLARIFICATION:

To prevent any further confusion and ensure a uniform application of the law, we kindly request your esteemed office to take this issue to the GST council for appropriate Redressal by issue of circular clarifying the position or suitable amendment to the provision to clarify the position.

This clarification should ideally confirm that the total pre-deposit for an appeal to the GST Tribunal should not exceed 30% of the tax demand as per the FA order, thereby reflecting the true intent of the GST Council's deliberations. If the request for such reduction and clarification of interpretation requires an amendment, the same may kindly be taken up for its due consideration by the GST council and needed amendment may be made in the Act based on council's recommendation.

We believe that such a clarification and a reduction in pre deposit will greatly aid taxpayers in understanding their obligations, reduce litigation, and foster a more transparent and equitable tax compliance environment.

Taking into consideration the hardships which may be caused, we the members of Karnataka State Chartered Accountants Association, on behalf of the entire Chartered Accountants community and also on behalf of the trade and industry in the state of Karnataka appeal to your good selves to kindly consider our above request.