Introduction: As we step into the dynamic world of Goods and Services Tax (GST) in 2023, businesses are navigating a landscape marked by continual evolution. The compliance journey has become more intricate, with new regulations, opportunities, and tools reshaping the way organizations manage their GST obligations. This comprehensive guide is designed to be your compass through the complexities, offering insights into critical aspects such as filing Annual Returns, exploring the latest enhancements, and seizing opportunities like the Amnesty Scheme. Whether you’re a seasoned taxpayer or a newcomer to GST, this guide will equip you with the knowledge needed to navigate the intricate web of compliance, ensuring not only adherence to regulations but also capitalizing on the benefits offered by the latest changes in the GST ecosystem. Join us on this journey through the nuances of GST in 2023, where compliance meets opportunity and understanding the intricacies leads to a seamless and empowered business experience.

Introduction: As we step into the dynamic world of Goods and Services Tax (GST) in 2023, businesses are navigating a landscape marked by continual evolution. The compliance journey has become more intricate, with new regulations, opportunities, and tools reshaping the way organizations manage their GST obligations. This comprehensive guide is designed to be your compass through the complexities, offering insights into critical aspects such as filing Annual Returns, exploring the latest enhancements, and seizing opportunities like the Amnesty Scheme. Whether you're a seasoned taxpayer or a newcomer to GST, this guide will equip you with the knowledge needed to navigate the intricate web of compliance, ensuring not only adherence to regulations but also capitalizing on the benefits offered by the latest changes in the GST ecosystem. Join us on this journey through the nuances of GST in 2023, where compliance meets opportunity and understanding the intricacies leads to a seamless and empowered business experience.

1. File your Annual Return in Form GSTR-9 and Form GSTR-9C before due date

i. Please file your Annual Return in FORM GSTR -9 and FORM GSTR-9C for F.Y. 2022-2023 Before Due Date: 31/December/2023

ii. Taxpayers required to file FORM GSTR-9: All GST taxpayers having Aggregate Annual Turnover above Rs 2 Crore (during F.Y. 2022-2023) except the following:

1. input Service Distributor .

2. TDS Deductor ,

3. TCS Collector

4. Casual Taxable Person

5. Non-Resident Taxable Person

iii. Taxpayers required to file FORM GSTR-9C: A self-certified reconciliation statement in FORM GSTR-9C needs to be filed along with Annual Return in FORM GSTR-9 by the taxpayers whose Aggregate Annual Turnover is above Rs 5 Crore (during F.Y. 2022-2023)

iv. Late Filing of Form GSTR-9 and Form GSTR-9C will attract late fees.

2. Small Businesses enabled to make supplies through e-Commerce Operators

Small Businesses enabled to make supplies through e-Commerce Operators w.e.f. 1st October 2023. This would open the huge e-commerce market for small businesses without getting mandatory GST Registration upto threshold turnover of registration.

- Unregistered suppliers and Composition Taxpayers are now allowed to make intra-state supplies through e-Commerce Operators (ECOs) w.e.f. 1st October 2023

- Lakhs of small businesses would be benefited from the waiver of requirement of mandatory registration for selling goods through e-Commerce Operators upto threshold turnover of registration

- This would open the huge e-commerce market for small businesses without getting mandatory GST registration upto threshold turnover of registration

- Extension of the benefit of making intra-state supply of goods through an e-Commerce Operator to the composition taxpayers shows government commitment to support small businesses.

For details please refer to the notification No. 34/2023-CT Dated 31.07.2023.

3. Special Amnesty Scheme for Condoning Delay in Filing GST Appeal

i. Who can apply under this Amnesty Scheme?

- The taxable persons who could not file an appeal, within the specified time period, against the demand order passed by the proper officer on or before the 31.03.2023, and

- The taxable persons whose appeal against the said order was rejected solely on the grounds that the said appeal was not filed within the specified time period

ii. To avail this Amnesty Scheme, you can now file an appeal in Form GST-APL-01 against the said order on or before 31.01.2024, subject to the payment of:

- Admitted liability (tax, interest, fine and penalty) arising out of the impugned order

- A sum equal to 12.5% of the remaining amount of tax in dispute out of which at least 20% should have been paid by debiting from the ECL

For details please refer to the notification No. 53/2023-Central Tax Dated 02.11.2023.

This is a golden opportunity for those taxpayers who might have missed the appeal deadline.

4. 2023: A Year of New Highs

Year 2023 has been a year of new highs in a single day, in terms of highest e-way bill generation, highest payment transactions, Highest Tax collection and Highest Return filing.

5. Enabling online compliance for liability & ITC mismatch

• The first feature lets taxpayers clarify variations in tax liability found by the tax department in their GSTR – 1 & 3B online filings.

• Taxpayers receive an intimation in the Form of DRC -01B. They can make the payment of the differential amount and for file a reply in Form DRC-01B, providing clarification.

• The second feature allows taxpayers to explain differences in Input Tax Credit between GSTR- 3B returns And GSTR-2B statements online.

• Taxpayers receive an intimation in the form of DRC-01C. They can pay the differential amount and /or file a reply in Form DRC-01C Part B, Providing clarification.

The above functionalities have automated the process of identifying mismatch in ITC/tax liability and have eased the process of compliance for taxpayers.

6. Enhancements in Form GSTR-3B

GSTR -3B return filing made Easier with enhancement in Form GSTR-3B and introduction of Electronic Credit and Re-claimed statement.

- The GSTR-3B format on the portal has been updated to help taxpayers accurately report information on ITC availed, ITC reversal, and ineligible ITC in Table 4

- A new ledger called Electronic Credit and Re-claimed statement was introduced to aid taxpayers in accurately reporting ITC reversal and reclaim. It helps track ITC reversed in Table 4B(2) and subsequently reclaimed in Table 4D(1) and 4A(5) for each return period, minimizing clerical errors

- Mechanism prescribed for reversal and re-availment of ITC in case of non-payment of Tax by the supplier

It facilitates the taxpayers in correct and accurate reporting of ITC reversal and reclaim thereof and to avoid clerical mistakes

7. e-Invoice

E-invoice verifier App introduced to provide a convenient solution for verifying e-invoices and other related details.

- For mandatory generation of e-invoice, the threshold limit of annual aggregate turnover reduced to Rs. 5 Crore w.e.f. 01.08.2023

- An e-invoice Verifier App was introduced to provide a convenient solution for verifying e-invoices and other related details.

- This app aims to simplify the process and provide an efficient and accurate e-invoice verification

- QR Code Verification allows users to scan the QR Code on an e-invoice to determine the authenticity of the e-invoice

8. Facility for transfer of balance in Electronic Cash Ledger (ECL) between the registered persons having the same PAN

- Unutilized balance in CGST/IGST head in Electronic Cash Ledger, can now be transferred between the registered persons having same

- PAN This facility will help in:

- Utlilizing balance in Electronic Cash Ledger

- No requirement of filing separate refund claim

- Promoting Ease of Doing Business

- Improving liquidity and cash flow of taxpayer.

For details please refer to the notification No. 34/2022-Central Tax Dated 05.07.2022.

9. GST is also helping MSMEs to get Credit/Business Loans

- "Account Aggregator" has been notified as the systems with which information may be shared by GST Portal based on consent provided by the registered person/taxpayer

- This will help MSMEs in getting credit/business loan based on their GST registration

For details refer to Notification no. 33/2023-CT dated 31.07.2023

10. Compliance Burden Reduced for Small Taxpayers

Requirements of filing Annual Return in FORM GSTR-9 has been waived off for taxpayers with annual turnover up to Rs.2 Crore in the F. Y. 2022-23.

For details refer to Notification no. 32/2023-CT dated 31.07.2023

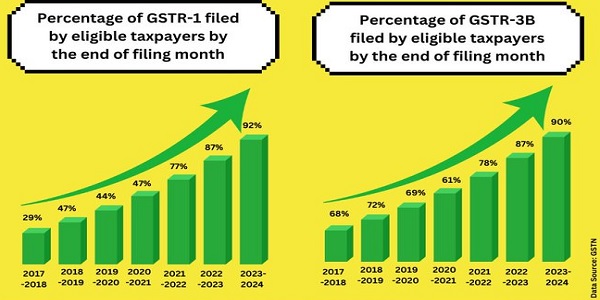

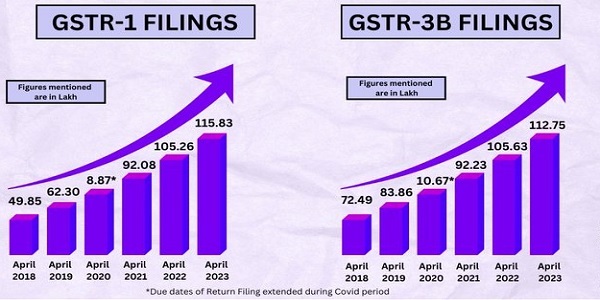

11. Simplification in Rules and Procedure in GST

Simplification in Rules and Procedure in GST has resulted in increase in return filing percentage by eligible taxpayers.

12. Growth in Return Filling

Improvement in Compliance Level

Increase in return filling across the years indicates improvement in compliance level

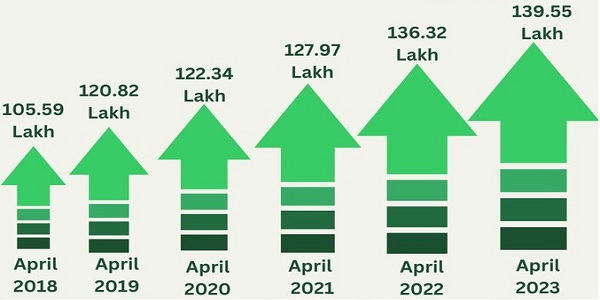

13. Increase in GST Taxpayers Base

Number of active taxpayers in GST system has shown an increasing trend across the years

(Data Source: GSTN)

Conclusion: Navigating the complexities of GST compliance is pivotal for businesses. In 2023, understanding the nuances of filing, embracing new opportunities, and leveraging simplifications can contribute to a seamless and compliant journey in the world of GST. Stay informed, stay compliant!